|

|

|

|

-

20 - Part 7 – Accounting

Credit Memos

With the Quantrac 2005 Accounts Receivable, you have the ability to create Credit Memos (or negative balance

invoices). In accordance with Generally Accepted Accounting Principles, you may create a credit memo

referencing an unpaid invoice. You may apply that CM balance to any outstanding invoice.

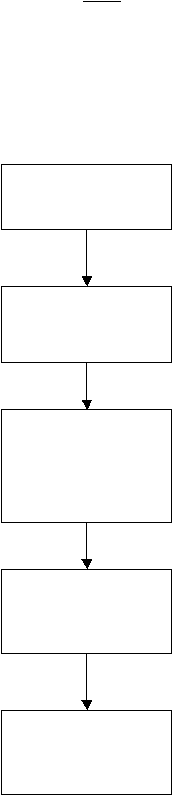

Flow Chart Example: The following flow chart is based upon the following hypothetical scenario.

Your company provides air conditioning service for a customer. An invoice is created and presented to the

customer. Before the invoice is paid by the customer, he/she changes his mind and decides to replace the repaired

unit, instead.

Using this scenario, you may create a credit memo for the full amount, tax, or any amount of either, thus effectively

nullifying the original transaction.

You provide the service

for a customer. You

present him with an

invoice.

When you create an invoice, the following GL Accounts are affected:

Revenue account increases (debit)

Sales Tax account increases (debit)

Accounts Receivable account increases (credit)

Customer later decides to

replace instead of the

already completed

repairs.

You create a Credit

Memo for part or all of

the original invoice.

Note: at this point, both

the original invoice and

the credit memo “live” in

your accounting system.

When you create a credit memo, the following GL Accounts are

affected:

Credit Memo Liability account increases

(debit)

Sales Tax account decreases

(credit)

Revenue Account Decreases

(credit)

If you print statements for

this customer at this

point, both the original

invoice and the credit

memo will appear.

To complete the cycle,

you must apply the credit

to the invoice. Upon

completion, they will have

cancelled each other.

When you apply the credit memo to an invoice, the following GL

Accounts are affected:

Credit Memo Liability account decreases

(credit)

Accounts Receivable account decreases

(debit)